Finwower is a leading advertising-supported and independent comparison service. Finwower receives a part of the revenue as compensation from all the offers that you see on the website from various companies. Depending on the compensation, you will see where and how the products appear on the website. For instance, you can look at how the order appears in the listing category. Of course, many other factors impact the appearance of the products, like the credit approval likeliness of the applicants and the rules of the proprietary website. Of course, it should also be understood that you will not find all the available credit or financial offers available today at Finwower.

All the reviews you see have been prepared by the staff of the Finwower. Yes, these opinions are received by the reviewer and have not been approved or reviewed by other advertisers. It means that all the reviews you see are unbiased and presented accurately, including the credit fees and rates. If you are looking for the latest information, it is suggested that you head over to the top of the page and visit the bank's website to check the data. All the credits at Finwower are determined from the FICO® Score 8; this is one of the many types of credit scores you will find in the market. When the lender is considering your credit application, they may use various types of said credit score to determine whether you qualify for the credit card or not.

What is business car insurance?

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here's how we make money.

Have you ever thought that your car insurance may not be taken out for the right reasons? You work hard for your money, so why should you beg the insurance company to cover you? You may be a victim of fraud. It is likely that you are unaware of this risk. You will find that most policies are sold through aggressive marketing campaigns that manipulate your emotions. With the help of RiskValue's experts, let's take a look at the elements of business auto insurance to give you a clear idea of what to expect and what to watch out for.

How does corporate auto insurance work?

Let's start with the most common examples of fraud in this type of insurance policy. One of the main perpetrators of fraud is the used car salesman. These may claim that the car is in perfect condition when, in fact, it has significant wear and tear. As a result, it does not meet the standards of a clean title and they know that you will not want to buy a vehicle with a damaged title. In addition, they will claim that the car needs minimal maintenance when, in fact, it requires a significant amount of work. This is how they will try to convince you to take out the policy. Most importantly, this is how they will try to keep you in their program. They will tell you that you can get a significant discount if you commit to keeping the car for five years or more. What they don't tell you is that, in fact, the five-year warranty lapses in the event of an accident or breach of contract. In other words, after the first five years you are on your own. It's called the duck game, and it's played on a large scale with insurance companies rather than individual owners. In fact, in 2019, Forbes ranked identity theft as one of the top ten personal security risks. It is a serious crime and its perpetrators will do anything to obtain your personal information. They may even pose as employees of your bank or insurance company to trick you into revealing your information. Considering that most identity theft scams occur online, it is clear that you are at risk. In most cases, thieves use fake documents and stolen identities to get what they want.

The benefits of buying from a trusted seller

When you buy a used car from a reputable seller, you can be assured that the vehicle has been thoroughly inspected. The seller wants to make sure that you are not taking a huge risk by buying a used car he knows nothing about. He wants to protect his investment and ensure that he will be reimbursed if you decide to return the vehicle. The inspection process will reveal any major problems with the vehicle. If you are looking for a reliable, durable and safe vehicle, you should consider buying a vehicle that has been inspected by a professional mechanic. This will ensure that your vehicle is properly maintained by someone who knows what he or she is doing. You can be assured that he or she will treat your car with the same care as he or she treats his or her own. After all, you are buying from someone he knows and who, if he knows you are a dangerous driver or have a criminal record, will try to avoid dealing with you. In most cases, the risk associated with buying a used car is negligible, but it does exist. In other words, you run a small chance that something will happen to the car you purchase. If you are looking for a reliable, durable and safe vehicle, you should consider buying one that has been inspected by a professional mechanic. That way, you can be assured that the vehicle will be properly maintained by someone who knows what he or she is doing. You can be sure that the mechanic will treat your car with the same care as he treats his own. After all, you are buying from someone he knows and who, if he knows you are a dangerous driver or have a criminal record, will try to avoid dealing with you.

The most aggressive marketing campaigns

Although the previous scenario is certainly bad, it is not the only risk you may face. In most cases, you will be faced with aggressive marketing tactics by insurance companies posing as good Samaritans who want to help you protect your car. In other words, they will try to convince you to take out an insurance policy as soon as possible so they can start generating profits from your insurance premiums. It is likely that you have seen advertisements on social media that try to push you into a no-win situation. They manipulate your emotions by leveraging your fears, using techniques such as fear mongering and urgency. In most cases, insurance companies will try to get you to sign up for an insurance policy within a few days so they can start generating profits from your insurance premiums. In most cases, they will want to get you to buy the bare minimum so that they can squeeze as much out of you as possible. After all, you are a potential source of profit for them.

In most cases, they will want you to purchase the minimum amount so that they can squeeze as much out of you as possible. After all, you are a potential source of profit for them.

Do not be fooled by this kind of sales maneuver. The only way to get a good deal, if that is your case, is to compare all the offers you receive in the mail. You will probably find that you often get the best price by comparing all the policies you receive in the mail rather than the one you hear about on social media. The reason is simple. Once you commit to purchasing a policy, the insurance company has the legal right to access your credit file and check your creditworthiness. In most cases, before offering you a good deal, they will want to make sure that you are a stable source of income. In other words, they do not want to waste their time with someone they know will eventually abandon them for lack of profit. In most cases, the best price is found when you compare all the policies you receive in the mail rather than the one you hear about on social media. The reason is simple. Once you commit to purchasing a policy, the insurance company is legally allowed to access your credit file and check your creditworthiness. In most cases, before offering you a good deal, they will want to make sure that you are a stable source of income. In other words, they do not want to waste their time with someone they know will eventually abandon them for lack of profit.

What should you pay attention to?

When comparing prices, watch out for any unusual fees or commissions that the insurance company might charge you. In most cases, the prices are all the same, or at least close. However, if you notice something, it usually means you are being charged an additional fee. For example, they may want to add an extra $5 to $20 to your car insurance premium. In most cases, this is a sign that they are charging you an additional fee for something you do not need, and this is your chance to say no. In most cases, you will be faced with aggressive marketing campaigns by insurance companies posing as good Samaritans who want to help you protect your car. Although this is a kind gesture, it usually means that they want to sell you more products than help you protect your car. In most cases, you get the best price by comparing all the policies you receive in the mail rather than the one you hear about on social media. The reason is simple. Once you commit to buying a policy, the insurance company has the legal right to access your credit file and check your creditworthiness. In most cases, before offering you a good deal, they will want to make sure that you are a stable source of income. In other words, they do not want to waste their time with someone they know will eventually abandon them for lack of profit. In most cases, the best price is found when you compare all the policies you receive in the mail rather than the one you hear about on social media. The reason is simple. Once you commit to purchasing a policy, the insurance company is legally allowed to access your credit file and check your creditworthiness. In most cases, before offering you a good deal, they will want to make sure that you are a stable source of income. In other words, they do not want to waste their time with someone they know will eventually abandon them for lack of income.

What types of car insurance are available to businesses?

Owning a car is essential, not only because it allows us to get around quickly and easily, but also because it is a form of self-protection. In the event of an accident or mishap, a personal vehicle can provide immediate relief from economic hardship. However, the coverage provided by the insurance policy can be quite confusing. In this article we will examine the different options available to businesses and entrepreneurs and the advantages and disadvantages of each type of coverage.

Personal insurance

This type of insurance covers your car and is the easiest form of insurance to understand. You are the named insured on the policy and the car itself is usually covered. Although it does not cover assets other than the vehicle or business assets, it protects you from most financial burdens, except for litigation and claims. Liability coverage, in particular, can be very high or even total, depending on the policy and how you use your car. The disadvantage of this type of coverage is that you are the one who has to pay most of the costs. For example, if your car is involved in an accident and the cost of repairs is $1,000, you will have to cover this expense. In case of a lawsuit, you will also have to hire a lawyer and pay the legal fees and associated risks. In addition, if someone sues you for an accident that occurred while you were driving your car for work, you could incur serious financial liability.

Commercial insurance

If you run a business of any kind, chances are you will need commercial insurance. Since its inception, the trucking industry has relied on commercial insurance policies to protect against the financial risks associated with running a trucking business. Generally speaking, the named insured is the entity legally responsible for operating the vehicle, i.e., you, as an individual, or a corporation. The amount of insurance coverage depends on turnover and the number of trucks on the road. The cost of this coverage can be very high, up to 10% of the total annual expense. This percentage can vary depending on the insured and the type of insurance.

The advantage of this type of insurance is that it allows the financial responsibility for accidents and mishaps to be spread over a larger authority. This is generally a good thing, as it removes stress from the financial equation. In most cases, business insurance includes a high level of liability coverage and a standard car damage waiver clause.

Protecting the company

Besides covering assets and liabilities, what else might your company need? Perhaps you need liability insurance for the products you sell. This type of insurance protects you and your company from lawsuits that could be brought because of a defective product you sold that caused damage or injury to people or property. In this case, you are the named insured and the car itself is not covered. It is the insurance company that covers the costs of your defense in court. This type of insurance is often referred to as product liability insurance.

The advantage of this type of insurance is that it allows you to limit your exposure to lawsuits. If you take out this type of insurance, you will benefit from product liability coverage in the event of a lawsuit. On the other hand, this type of insurance requires constant maintenance, as you need to monitor the details of each claim and defense.

Motorcycle accident insurance

If you use a motor vehicle as part of your business, you may want to consider motorcycle accident insurance. This type of insurance provides coverage in the event of an accident or mishap while riding a motorcycle. Generally speaking, the named insureds are the people legally responsible for driving the vehicle, i.e., you as an individual or as a company. The cost of this coverage is relatively low, generally between 3% and 6% of the total liability coverage. This cost can be offset by a lower premium than other forms of business insurance.

In addition, motorcyclists are generally more aware of their surroundings than drivers of other vehicles. This awareness can reduce the risk of accidents and mishaps. In addition, motorcycles are becoming increasingly popular as an everyday means of transportation, which means that there are more people who can be held liable in the event of an accident. It also means that there are more opportunities for lawsuits, giving you the chance to get compensation under your insurance policy. The disadvantage of this form of insurance is that it can be quite expensive, given the limited scope of coverage and the fact that you are not protected in case of theft or burglary.

Liability insurance for alcoholic beverages

If you sell or serve alcohol on your premises, you might consider taking out alcoholic beverage liability insurance. Like motorcycle accident insurance, this type of insurance provides coverage in the event of a lawsuit or other legal action as a result of an accident or mishap while selling or serving alcoholic beverages. The insured named in this type of policy is the individual or legal entity that is legally responsible for operating the premises. Although this type of insurance generally covers accidents that occur in bars, it can also be used to protect against injuries caused by those driving or walking while intoxicated or under the influence of alcohol.

The cost of this type of insurance may vary depending on your state's alcohol licensing requirements. In most cases, however, it represents only a small part of the cost of commercial insurance. On the other hand, the limitation of coverage is similar to that of commercial insurance in that it does not cover your property or other vehicles associated with the business. Also, if you do not have a pub license, you cannot take out this form of insurance, as it is considered a public nuisance if you do not have the required license.

What about rental car insurance?

If you occasionally rent a car for business purposes, you might consider taking out rental car insurance. If, while using a car, an accident or mishap occurs that is not covered by your insurance, this form of insurance may be the solution. Usually, the named insured under this type of policy is the person or company who is legally responsible for the use of the rented car. In most cases, the car itself is not covered, only the person renting it. The cost of this insurance can be quite high, usually 10-20% more than normal commercial insurance. However, in case of an accident or mishap, it can be a lifesaver.

On the other hand, this type of insurance allows you to protect your property in case of accident or mishap. In most cases, rental insurance includes a high level of liability coverage and a standard waiver of recovery clause in the event of an emergency or collision. This emergency or collision waiver clause allows you to choose whether or not to participate in an emergency compensation program, which can be useful if you are going through a difficult time and cannot afford to lose potential income. This form of insurance is ideal for frequent travelers who need to protect their investment in a rental car.

The disadvantage of this type of insurance is that you have to inform your insurer immediately after each trip. This means that you have to remember to inform him every time you rent a car, which can be difficult. Another disadvantage is that you have to take out additional liability insurance if you rent a car worth more than $25,000 or if you transport goods worth more than $10,000. Finally, if you have an accident while driving a rental car, you should inform your insurance company as soon as possible. Don't forget to seek the advice of an attorney familiar with these types of insurance policies before making any decisions.

How do you add business insurance to a car?

Do you drive a car that is worth a lot? If so, you should consider adding business insurance to your vehicle. There are several reasons why you should consider this option. For example, if you have a lot of your company's stock in your vehicle, you should consider taking out accident insurance, because you could lose a lot of money. Another reason is that you own a small business and need extra coverage for liability reasons. Finally, you may want to add commercial insurance to your car because you appreciate the extra freedom of being able to go where you want, when you want, without having to worry about legal problems. The list of benefits goes on. So let's see how to add commercial insurance to your car.

Getting a quote

The first step in adding business insurance to your car is to gather information about your current coverage and calculate the amount of additional insurance you will need. The best way to do this is to contact an insurance agent or get a quote from several agents. Getting a quote is often a frustrating experience, so you should do your best to find a competent and friendly agent. Once you find an agent you trust, ask him or her to help you get a quote for the amount of coverage you need. When writing the quote, don't forget to mention that you need commercial insurance and try to get an answer that takes into account the use you will make of your car.

Choosing a policy

Once you have the quote, you need to start comparing different policies to choose the one that best suits your needs. In many cases, the best auto policy is one that covers both liability and property damage. Liability insurance protects the driver in case of bodily injury or property damage. The main types of liability you will face as a business owner are traffic accidents, medical malpractice and defective products. You need to look for a policy that best covers these costs and liabilities and gives you the protection you need. If you plan to use your car for business, you can also take out an additional policy that covers your business equipment (laptops, cell phones, etc.). Property damage insurance protects you if your car collides with another car or heavy equipment. For example, if a coworker hits the back of your car and causes damage, you will need property damage insurance to repair it. Make sure your liability and property damage insurance policies have a minimum coverage of $100,000 for liability and $100,000 for property damage. In many cases, this amount of coverage is sufficient for small businesses. If you have a larger business, you may want to consider additional policies to meet your needs. Keep in mind that insurance policies can and often do vary from state to state, so it is essential to compare several policies before making a decision. In the "Resources" section at the end of this article you will also find a link to a State Farm agent's website.

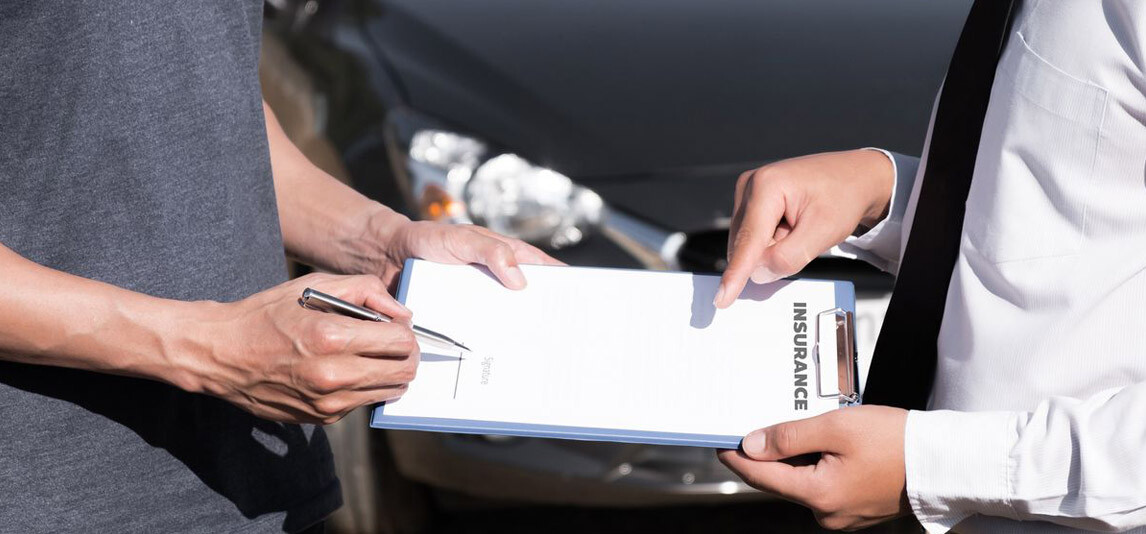

Signing the documents

Once you have made the decision to purchase insurance for your car, the next step is to have the documents prepared by a notary public or insurance agent. Have the documents notarized before they are certified to ensure the validity of the insurance policy. If you use an agent, ask him or her to do all the paperwork for you. If you are responsible for obtaining adequate insurance coverage, it is important to have the documents signed as soon as possible. Otherwise, the insurance company may deny your claim on the grounds that the coverage was not in effect at the time of the claim. If you are self-insured and have a policy that you think will be cancelled because of the new coverage, call your agent immediately to have it reinstated. Don't forget to keep proof of your insurance coverage throughout the year in case you are asked for it by the police or a traffic agent. In the event of an accident or theft, officers may ask you about your insurance. It is also advisable to keep copies of all relevant documents in a safe place in case they are needed in the future.

Verification of coverage

Once you have all the necessary documents in hand, it is finally time to check the coverage of your policy and assess the level of protection you have. Remember that coverage may vary from state to state. You can also call the insurance company directly to get the details of your coverage, state by state. When you call, be sure to ask for a copy of your insurance policy and a list of items covered by the policy. It is very important to check your coverage, especially if you are not familiar with it or if you decide to cancel it. You should do this at least once a year, and if you find that the coverage is incomplete or that there are gaps, you should contact your agent or insurance company as soon as possible to have the coverage corrected.

Protect your investment

Even if you do not use your car for business purposes, you probably consider it a valuable asset. It is therefore natural that you want to protect your investment. One way to do this is to add business insurance to your car. If you are driving a car that is worth a lot, you should probably consider adding business insurance to your vehicle. There are many reasons for this. For example, if you have a lot of your company's stock in your car, you should consider adding business insurance because you could lose a lot of money. Another reason is that you own a small business and need extra liability coverage. Finally, you may want to add commercial insurance to your car because you appreciate the extra freedom of being able to go where you want, when you want, without having to worry about legal problems. The list of benefits is endless. So let's look at how to add commercial insurance to your car.